Top Stock Ideas For 2018 Part 3

Oil is a Great Contrarian Play

I want to start Part 3 of my top stock ideas for 2018 by taking a look at a chart of West Texas Intermediate Crude. This is the US benchmark crude price. As can be seen in the chart the trend is up as oil has been strengthening in price since this summer.

I believe that this will continue into 2018 and will catch many analysts and investors by surprise. The reason that many will be caught by surprise is because of a psychological factor known as normalcy bias.

Most people look at tomorrow and assume it will pretty much be like today. They assume this because today was pretty much like yesterday (normalancy bias). This works for most things in our life except speculating and investing in markets. We are currently experiencing normalancy bias in the oil markets. The oil oversupply situation has been ongoing for so long most investors expect that it will continue.

Market Assumptions

The market narrative as it applies to oil for the last several years is that due to fracking and improved drilling completion techniques, the US is now on its way “energy independence” whatever that means. This “energy independence” will finally free us of dependence on foreign oil and the troublesome middle east.

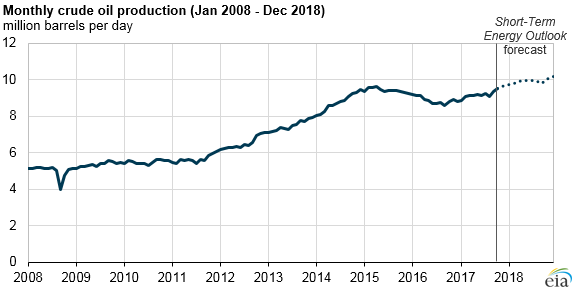

It is a fact that fracking and technology have increased oil production due primarily to newly exploited shale areas.

Shale Oil The Reality

However it appears that historically low interest rates have created a bubble in these shale plays. A recent article by Steve St. Angelo at Goldseek.com illustrates this fact. Mr St.Angelo took a look at some of the larger players income statements and cash flow statements and discovered that all of them are cash flowing less than they are spending on drilling.

Is Shale Oil A Net Destroyer of Capital?

Some of these companies have used debt in the case of Continental Resources or asset sales in the case of Chesapeake Energy. Quote from the article:

A few minutes into the Bloomberg video, both Pioneer Resources Chairman, Scott Sheffield, and Continental Resources CEO, Harold Hamm, explain how advanced technology will revolutionize the shale oil industry and bring down costs. I find that statement quite hilarious as Continental Resources and Pioneer continue to spend more money drilling for oil and gas then they make from their operations. As I stated in a previous article, Continental Resources long-term debt ballooned from $165 million in 2007 to $6.5 billion currently. So, how did advanced technology lower costs when Continental now has accumulated debt up to its eyeballs?

Of course… it didn’t. Debt increased on Continental Resources balance sheet because shale oil production wasn’t profitable… even at $100 a barrel. So, now the investor who purchased Continental bonds and debt are the Bag Holders.

The Party Is Over

Low interest rates and hype have once again come together to create another bubble in our economy. Of course the shale oil bubble popped a couple of years ago when the Saudis decided to flood the market with oil.

This has resulted in once bitten twice shy attitude towards many of these companies. There will not be a lot of interest in high yield junk bonds to finance cashflow negative shale wells especially in a rising interest rate environment. Even if oil goes back to $100 per barrel. Equity raises? Forget it at current share price.

Price is Directly Related to Inventory Levels

While researching the oil markets I became intensely focused on finding what was really driving oil prices. Was it the drilling rig count? Geopolitical concerns? Putin?

After searching for weeks I stumbled upon the idea that inventory levels were driving oil prices. There is a small natural resources fund called Goehring & Rozencwajg. The firm publishes some outstanding research regarding drivers of the oil price. I suggest anyone involved in the resource market bookmark the site and read their research.

Goehring & Rozencwajg’s research is suggesting that industry analysts are underestimating oil demand and that OPEC is restricting supply sufficient to cause a reduction in oil inventories that will drive oil prices substantially higher. From their third quarter report:

Since we first wrote in January, inventories have not remained at record levels (the bear’s argument), but instead have drawn sharply just as our models predicted. In fact, since the end of February, US core petroleum inventories have drawn by nearly 500,000 b/d relative to long-term averages, while total OECD inventories (a proxy for global inventories) have drawn by 700,000 b/d relative to long-term averages. The total overhang relative to average levels has now repaired itself by 40-50% in only six months and our models continue to tell us inventory drawdowns will persist into 2018.

(skip)

However, our models tell us the days of investor complacency are quickly coming to an end. Energy analyst Mike Bodell has long followed the relationship between comparative inventory levels (i.e. the level of inventories relative to the long-term average) and the price of crude. The results have profound implications for today’s oil market. As we mentioned in our introduction, US core comparative inventories stood at ~200 mm bbl above long-term averages at the beginning of 2017. As the year has progressed, US core petroleum inventories have worked off nearly 40% of their overhang and now stand at ~88 million barrels. According to our models (which have accurately predicted the inventory draws to date), US core petroleum inventories should hit 20 million barrels by February 2018, at which point historically oil prices begin to move sharply higher. In fact, since 2007 when US core petroleum inventories have been within 20 million barrels of normal, the oil price has averaged $92, and has exceeded $75 per barrel 80% percent of the time. These trends are not limited to the US. On a global level, total OECD comparative inventories will reach 20 million barrels by the 2 nd Q of next year, which also suggests much higher prices.

The Goehring & Rozencwajg report was published 10/20/17 and oil inventories continue to decrease. This should continue as US shale continues to struggle and OPEC recently committed to extending their production cuts through the end of 2018.

Art Berman of Labyrinth Consulting Services, Inc has also come to the same conclusion and has an excellent presentation with colorful charts that show the correlation between comparative inventories of oil and the price. Click here for link.

What About Demand

Demand continues to grow. We are now experiencing a period of world synchronized economic growth for the first time in years. Oil demand, especially in developing markets is growing.

Global consumption rose by 1.6 million barrels per day (MMbbl/d) in 2016 and 2.0 MMbbl/d in 2015 as low prices and a synchronized economic expansion in most areas of the world spurred demand.

Consumption is forecast to increase by a further 1.6 MMbbl/d this year and 1.4 MMbbl/d in 2018, according to the International Energy Agency. And predictions have been consistently revised higher as demand data has come in stronger than forecast.

How to Play Oil

Ok so we have supply decreasing and demand increasing. Sentiment is still pretty bearish towards oil among many investors and speculators.

I am hesitant to buy many shale oil producers because of the fact that it is difficult to understand whether or not they can actually make money at any price level.

I like various service companies. They have been completely beaten down and are currently priced like they will be going out of business. As I have outlined above I expect the oil price to increase next year. This should change sentiment and capital will flow into these under owned names.

I specifically Like offshore oil driller Ensco (ESV). Another service company I like is TMK Group (TMKXY) which is Russian maker of drilling and pipeline pipe products. I did a write up on them recently on Seeking Alpha.

One oil producer that I do like is junior company Jericho Oil Corp (JCO.V) (JROOF). This small company has properties in Oklahoma. I like this company due to the prudence of management. The company spent the oil bust going around Oklahoma buying distressed acreage at cheap prices. Now that oil prices are increasing they should be able to bring on some lower cost production. True contrarians.

Speaking of Russia

I think buying the Russian market via the Russia ETF (RSX) could be a great play on oil. The Russian economy is heavily skewed towards energy and as the oil price recovers I would expect the Russian economy to benefit as it has in the past. There is a reason Senator John McCain quipped that Russia was a gas station next to gun shop built in the middle of a wheat field. The kicker is that the Russian stock market is one of the cheapest ones in the world based on CAPE valuation.

Oil Investment Is Lacking

In conclusion it now appears that oil is heading higher next year. I would also suggest that the price will over correct on the upside. This can be expected due to the investment gap that low prices have created. Oil is a depleting asset and the world requires hundreds of billions of dollars every year in new investment to find and develop new barrels to replace the barrels that have been produced. This has not happened. Oil is the lifeblood of modern civilization and the price will be going higher in 2018.

You can read Part 1 and Part 2 by clicking on the links

If you find my writing interesting I encourage you to susbscribe to my newsletter “Actionable Intelligence Alert”. In every issue I discuss various ways to capitalize on contrarian and overlooked investment ideas. Check it out by clicking here.